Study Material & Notes-Partnership Fundamentals – Sample page

Study Material & Notes for the Chapter 2

Partnership - Fundamentals

I. PARTNERSHIP BASICS

A. Partnership-Definition

The Indian Partnership Act 1932, Section 4

“Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all.”

Relation between persons

Who have agreed (written/oral)

To share the profits (losses)…business with a motive to earn profits

Of a business…legal business (theft/cheating, scam)

Carried on by all or

Any of them acting for all

B. Nature of Partnership

C. Nature of Partnership

To share profits in an agreed ratio

To take part in the conduct of the business

Right to be consulted

Right to inspect the books of accounts

Right to retire from the firm

To disallow admission of new partners (Imp).

Example 40 partners, want to admit new partner, one partner says No

D. Contents of Partnership Deed

Partnership agreement is the mutual understanding on which Partners decide to do a legal business to earn profits.

It may be oral or written.

The written, signed and registered version of the agreement is also called partnership deed

Deed is optional/non mandatory/non compulsory but recommended

Profit will be distributed/apportioned as per the agreement

Agreement once made needs to be honoured in all the conditions

The Partnership Deed may contains basically two types of matters:

Management related matters

Money related matters

E. Provisions relevant for Accounting

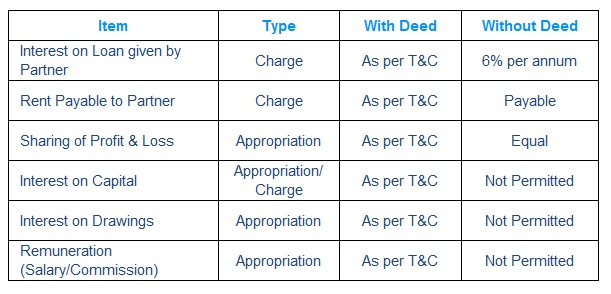

F. Interest on Loan given by Partner

Is a charge against profit (accrued even if no Profits)

Interest rate is as provided in the Partnership deed

If no partnership deed or not provided in partnership deed – @6% p.a.

Interest = Amount of Loan X Rate of Interest X Time

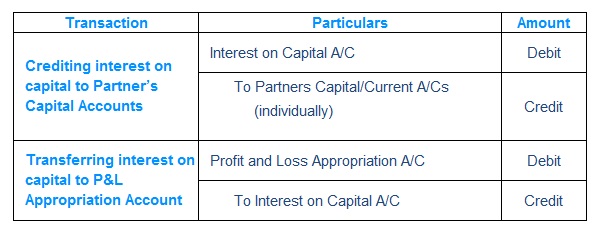

Interest is credited to Partner Loan Account (and not to Partner Capital/Current A/C)

Journal Entry

G. Rent Payable to Partner

Is a charge against profit (accrued even if no Profits)

Charge since rent is paid for using property for business purpose

Rent is credited to Rent Payable Account (and not to Partner Capital/Current A/C) Capital/Current A/C)

Journal Entry

H. Remuneration to Partner – Salary/Commission

Payable only if provided in the partnership deed

If loss – it is not payable, If sufficient profits – Fully allowed

If insufficient profits – Profits are distributed in the ratio of Salary/Commission to be allowed

Salary/Commission is credited to Partner’s Capital/Current Account

Journal Entry

II. INTEREST ON CAPITAL AND DRAWINGS

A. Interest on Capital

Interest is computed on time proportion basis, number of days capital deployed in Firm

Interest is computed only on Opening Capital, Additional Capital & drawings against capital

Interest is not computed on Profit/Loss

Interest on Capital= Amount of capital X Rate of Interest X Time

If only Closing Capital is given, interest cannot be computed on Closing capital

We need to find out Opening Capital and capital additions/deletions

If Opening Capital is not given prepare Capital A/C or use formula

Opening Capital=Closing Capital + Loss + Drawings- Profit – Additional Capital

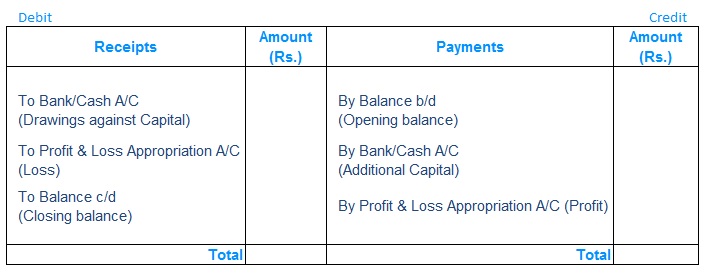

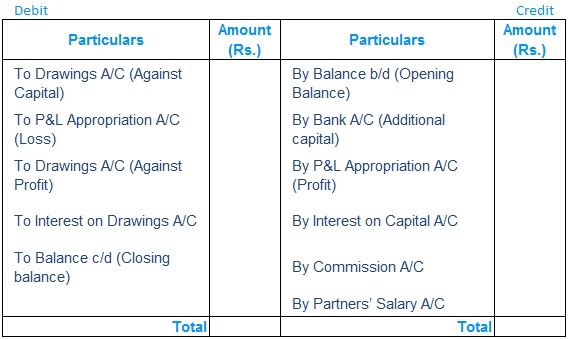

Prepare Ledger Account as per the below format

Partner Capital Account

For the year ended …………………….

Journal Entry

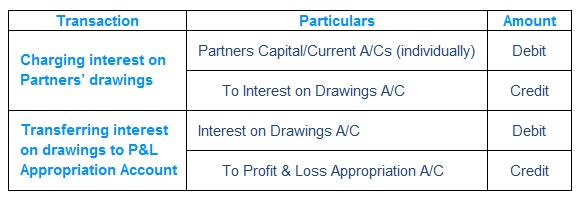

B. Interest on Drawings

Product Method (unequal amount withdrawn at different dates)

Simple Method – Interest is computed for each drawing separately using simple interest formula:

Product Method – Interest is computed for each drawing separately using simple interest formula:

Product = Each Drawing x No. of Months till Financial year end

Average Period Method (Uniform drawings & uniform time internal)

Two prerequisites / condition of using this method

Uniform/Similar time intervals…monthly, quarterly, half-yearly etc.

Uniform/Similar amounts on each interval say 1000, 5000, 10000 etc.

Important to Note:

If date of withdrawal is not given, the interest on total drawings for the year is calculated for six months on the average basis

When rate of interest is given without the word ‘per annum’ interest is charged without considering the time factor.

Journal Entry

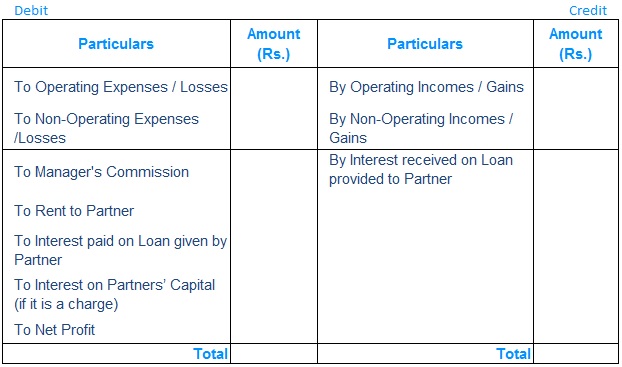

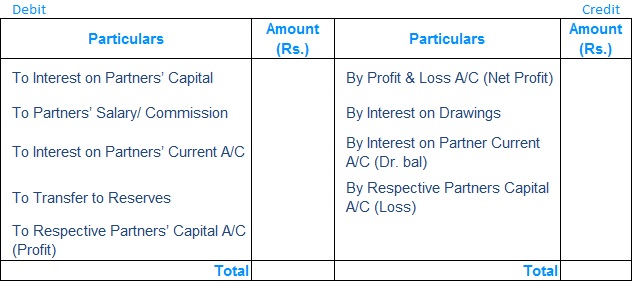

III. PROFIT & LOSS APPROPRITATION ACCOUNT

Profit & Loss Account

Profit & Loss Appropriation Account

Appropriation > Available Profits

Profit is distributed in the ratio of appropriations to be made, determined as follows:

Determine the amount payable as appropriation to each partner as per the Partnership deed (e.g. Salary, commission, interest on capital)

Total the amount of appropriations for each partner separately

The ratio of total appropriations amongst partners becomes the ratio for distribution of available profits among the partners

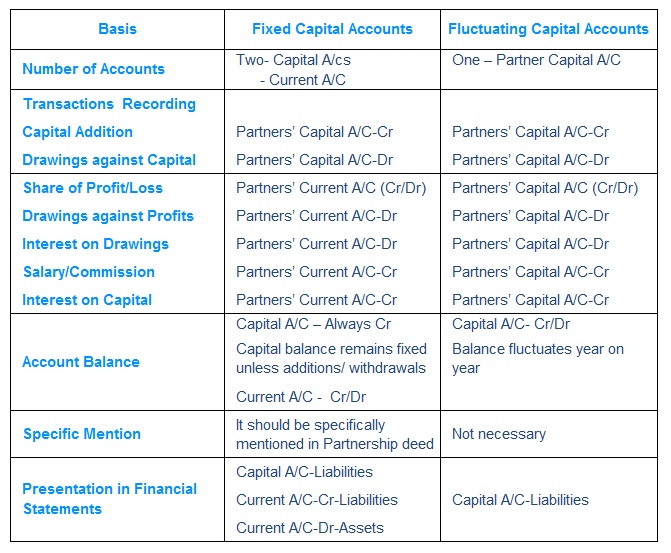

IV. FIXED AND FLUCTUATING CAPITAL

Capital Accounts

A. Fixed Capital

Partners’ Capital Accounts

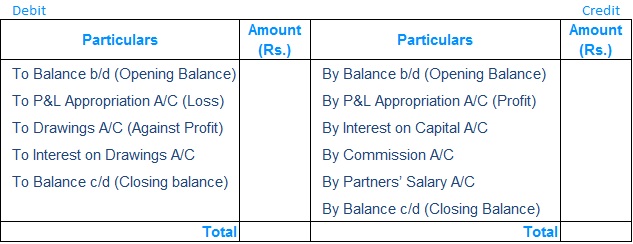

Partners’ Current Accounts

B. Fluctuating Capital

Partners’ Capital Accounts

A. Fixed Capital Ledgers

Partners’ Capital Accounts

Partners’ Current Accounts

B. Fluctuating Capital Ledgers

Partners’ Capital Accounts

C. Difference between Fixed & Fluctuating Capital Methods

In the absence of any information, always prepare fluctuating A/C

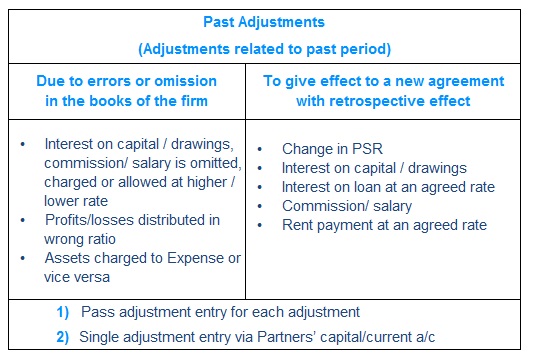

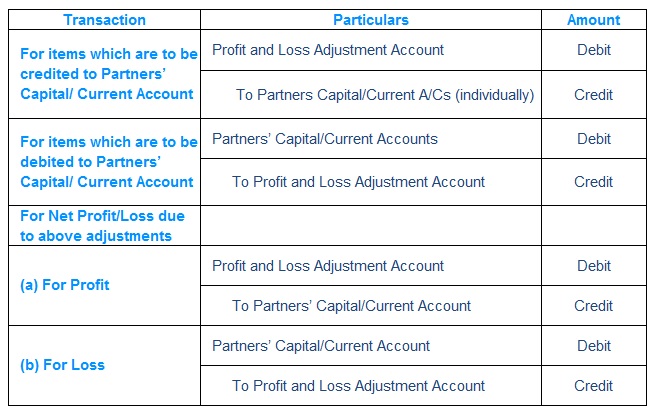

V. PAST ADJUSTMENT

Method-1 When net impact is routed through partners accounts

Process Steps

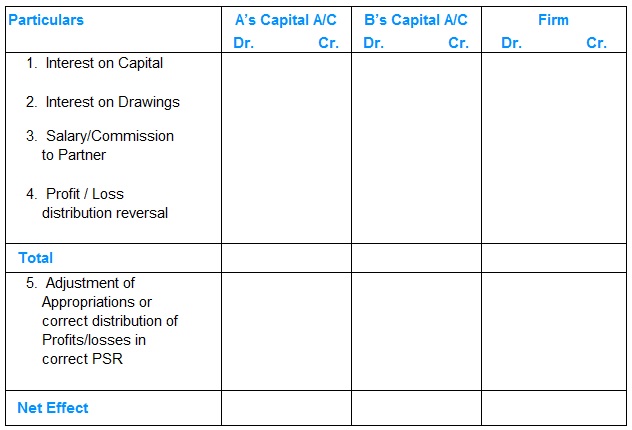

Prepare an analytical table in the following format

Benefits to partners are mentioned on credit side of respective Partner column and on the debit side of firm and vice versa

Total of columns designated to firm will give Firm’s net profit/loss

Distribute the profit/loss in profit sharing ratio

Sum partners columns and compute difference of total debit and total credit

If net difference is debit, that partner’s capital account will be debited and vice versa

Journal Entry

Method-2 Adjustment entry for each adjustment

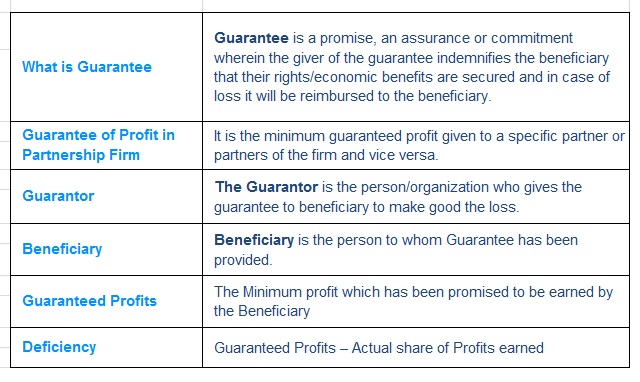

VI. GUARANTEE OF PROFITS

A. Definitions

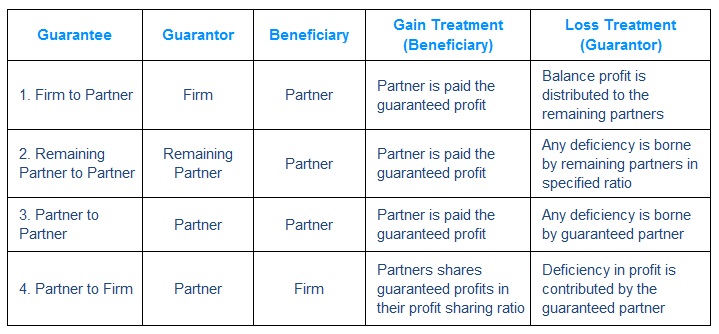

B. Type of Guarantees

C. Order of applying Guarantees

In case in a question two or more Guarantees are to be applied then this order is to be followed

By Partner To Firm

By Firm to Partner

By Partner to Another Partner(s)

When beneficiary’s actual share of profit is more than the guaranteed amount, then his share of profit is given to him, not guaranteed amount of profit.