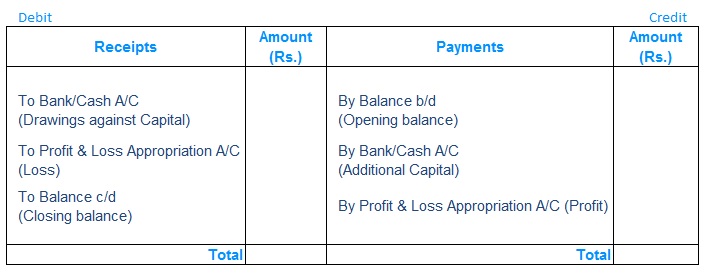

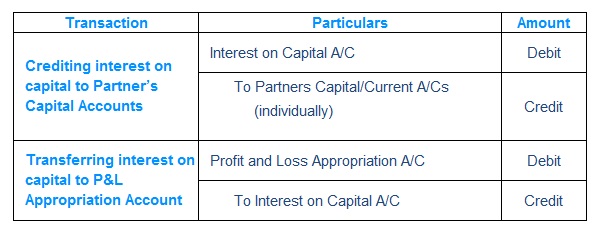

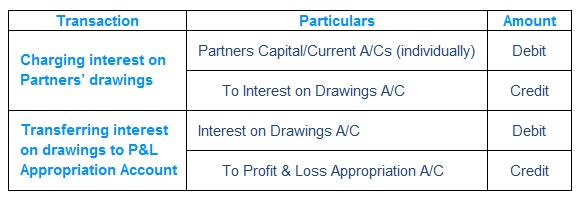

Partnership Fundamentals Notes2 Study Material & Notes for the Chapter 1 Partnership - Fundamentals II. INTEREST ON CAPITAL AND DRAWINGS A. Interest on Capital Interest is computed on time proportion basis, number of days capital deployed in FirmInterest is computed only on Opening Capital, Additional Capital & drawings against capitalInterest is not computed on Profit/LossInterest on Capital= Amount of capital X Rate of Interest X TimeIf only Closing Capital is given, interest cannot be computed on Closing capitalWe need to find out Opening Capital and capital additions/deletionsIf Opening Capital is not given prepare Capital A/C or use formulaOpening Capital=Closing Capital + Loss + Drawings- Profit – Additional CapitalPrepare Ledger Account as per the below format Partner Capital Account For the year ended ……………………. Journal Entry B. Interest on Drawings Product Method (unequal amount withdrawn at different dates) Simple Method – Interest is computed for each drawing separately using simple interest formula: Product Method – Interest is computed for each drawing separately using simple interest formula: Product = Each Drawing x No. of Months till Financial year end Average Period Method (Uniform drawings & uniform time internal) Two prerequisites / condition of using this methodUniform/Similar time intervals…monthly, quarterly, half-yearly etc.Uniform/Similar amounts on each interval say 1000, 5000, 10000 etc. Important to Note: If date of withdrawal is not given, the interest on total drawings for the year is calculated for six months on the average basis When rate of interest is given without the word ‘per annum’ interest is charged without considering the time factor. Journal Entry