IV. ISSUE OF DEBENTURES FROM REDEMPTION POINT OF VIEW

Redemption of debentures means repayment of the amount of debentures by company

Debentures can be issued at Par, Premium or Discount

Debentures can be redeemed at Par or Premium

Hence there are six combination possible as depicted in the figure below

2. Debentures issued at Premium and Redeemable at Par

(Issued at Rs. 125/- and Redeemed at Rs. 100/-)

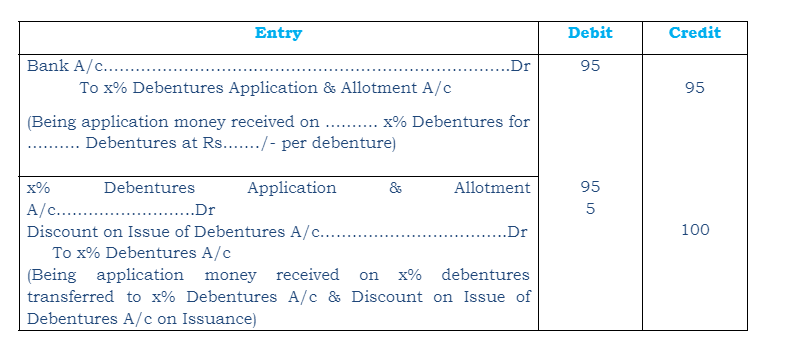

3. Debentures issued at Discount and Redeemable at Par

(Issued at Rs. 95/- and Redeemed at Rs. 100/-)

Discount on issue of debentures is netted off from Securities Premium Reserve (if it exists) or from the Statement of Profit & Loss Account in the year debentures are allotted

4. Debentures issued at Par and Redeemable at Premium

(Issued at Rs. 100/- and Redeemed at Rs. 110/-)

The liability of Premium on redemption arises the time of redemption of debentures. Being a known lability, following the prudence concept it is recorded on allotment of debentures itself

5. Debentures issued at Premium and Redeemable at Premium

(Issued at Rs. 125/- and Redeemed at Rs. 110/-)

6. Debentures issued at Discount and Redeemable at Premium

(Issued at Rs. 95/- and Redeemed at Rs. 110/-)

Disclosure in the Balance Sheet

Case-A Debentures are due for redemption after 12 months/operating cycle from the Balance Sheet date

Balance Sheet

Debentures will be shown under the heading ‘Long-term Borrowing’

Premium on Redemption of Debentures will be shown under the heading ‘Other Long-term Liabilities’

Case-B Debentures are due for redemption within 12 months/operating cycle from the Balance Sheet date

Debentures will be shown under the heading ‘Short-term Borrowing’

Premium on Redemption of Debentures will be shown under the heading ‘Other Current Liabilities’