II. CALCULATION OF PROFIT UP TO THE DATE OF DEATH OF A PARTNER

If the death of a partner occurs during the year, the representatives of the deceased partner are entitled to his/her share of profits earned till the date of his/her death. Such profit is ascertained by any of the following methods

Time Basis

Turnover or Sales basis

A. Calculation of Profit up to the Date of Death of a Partner – Time Basis

It is computed either on Previous Year Profit or Average Profit

Deceased Partner’s Share of Profits = Previous Year Profit X Time Till Death X Deceased Partner’s Share

12 or 365

Or

Deceased Partner’s Share of Profits = Average Profit X Time Till Death X Deceased Partner’s Share

Where, Average Profit = Total Profit

12 or 365

No. of Years

B. Calculation of Profit up to the Date of Death of a Partner – Sales or Turnover Basis

Deceased Partner’s Share of Profits = Last Year Profit X Sales Till Death X Deceased Partner’s Share

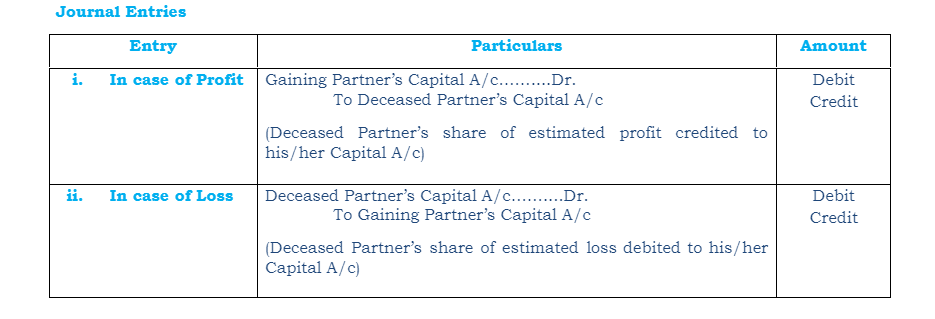

C. Accounting Treatment of Deceased Partner’s share in Profits

a) Through Profit & Loss Suspense Account – When New Profit-Sharing Ratio of the continuing partners does not differ from Old Profit-Sharing Ratio

b) Through Capital Transfer – When New Profit-Sharing Ratio of the continuing partners differs from Old Profit-Sharing Ratio