The new partner acquires his/her share of profit from the existing partners. This will result in the reduction of the share of existing partners. Therefore, the existing partners asks for Compensation for sacrifice of their profits, he/she compensates the existing partners for the sacrifices this compensation is called Premium for Goodwill. He/she compensates them by making payment in cash or in kind. The payment is equal to his/her share in the goodwill.

B. Premium for Goodwill

Premium for Goodwill = Goodwill of the Firm X New Partner’s Share

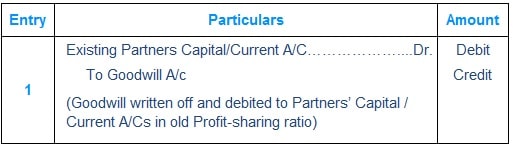

If Goodwill is already appearing in the books

As per Accounting Standard-26 (AS-26), goodwill can be recorded/debited in the books only when some consideration in money or money’s worth has been paid for it. Thus only purchased goodwill should be recorded in the firm’s books

If at the time of admission of a new partner, goodwill is appearing in the Balance sheet of a firm, it would be desirable to close the Goodwill Account

Journal Entries

C. Premium for Goodwill – Various Scenarios

All good firms take necessary safety precautions and train their workmen to avoid any accidents

At the factories/workplace despite all safety precautions and training there may be a situation wherein a worker might meet an accident resulting into medical treatment or disability.

Since the accident taken place at the Firm’s premises, there is a claim from the workmen/employee

To meet such contingencies, good firms generally set aside funds and create specific reserve Workmen Compensation Reserve

Any claim from workmen is paid out of the Workmen Compensation Reserve

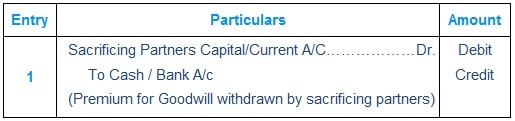

If Premium For Goodwill withdrawn by the existing partners

Journal Entries

Important to Note: The Assets and Liabilities remain at the book value. No adjustment in the Balance Sheet of the revalued assets/liabilities

D. Hidden Goodwill

Firm’s Goodwill = Total Capital – Net Worth

Where:

Total Capital = New Partner’s Capital X Reciprocal of New Partner’s share

Net Worth = Adjusted Existing Partners Capital + New Partner’s Capital

Computation of Net Worth (Liabilities Side Approach) = Existing Partner’s Capital + Free Reserves + Revaluation Profit – Revaluation Loss – Accumulated Losses – Existing Goodwill – Fictitious Assets

Computation of Net Worth (Assets Side Approach) = Total Assets – Outside Liabilities + Revaluation Profit – Revaluation Loss – Accumulated Losses – Existing Goodwill Fictitious Assets

Premium For Goodwill = Goodwill of the Firm X New Partner’ Share